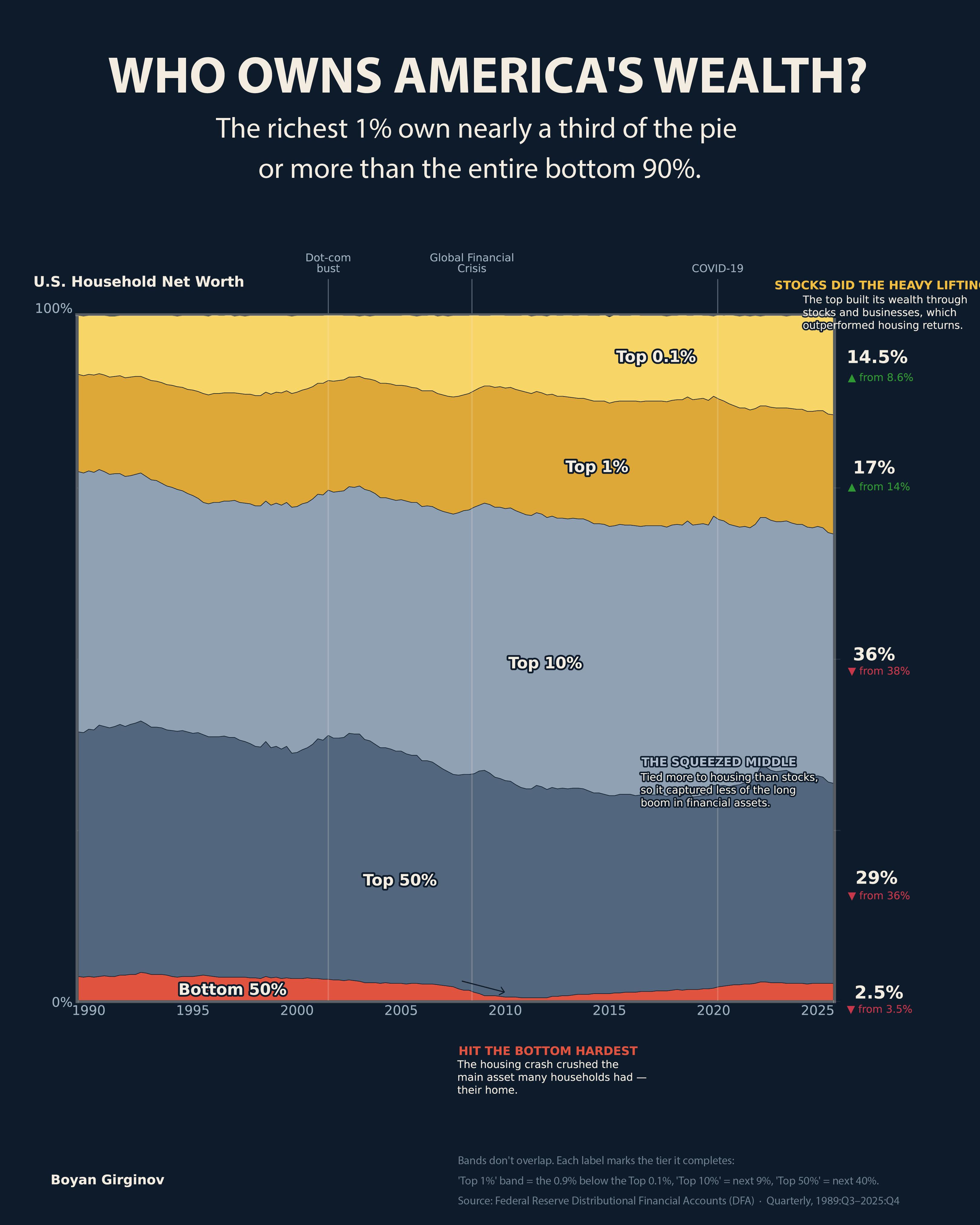

Für Amerikas Wohlstandsgefälle gilt eine einfache Regel:

Besitzen Sie Vermögenswerte oder beobachten Sie, wie sich die Kluft vergrößert.

Die oberen 0,1 % besitzen jetzt 14,5 % des gesamten US-Haushaltsvermögens.

Das ist fast 6x der Anteil, der den gesamten unteren 50 % gehört.

Und seit 1989 haben die obersten 0,1 % ca. erobert zwei Drittel Anteil am Vermögenszuwachs des obersten 1 %.

Der Grund ist einfach:

- Die Spitze besitzt mehr Aktien, Fonds und Privatunternehmen.

- Die Mitte besitzt mehr Wohnraum.

- Die Unterschicht besitzt sehr wenig Nettovermögen.

Wenn also die Märkte boomen, steigt die Vermögenskonzentration.

Wenn es auf dem Immobilienmarkt zu Zusammenbrüchen kommt, trifft es Haushalte mit geringerem Vermögen am härtesten.

Deshalb war 2008 so wichtig: Der Immobiliencrash hat das Vermögen der unteren Hälfte fast ausgelöscht, während die Erholung die Finanzanlagen, die sich größtenteils im Besitz der oberen Hälfte befinden, in die Höhe getrieben hat.

Die Vermögenslücke ist nicht nur eine Einkommensgeschichte.

Es ist eine Eigentumsgeschichte.

Von ExaminationOk6652

31 Kommentare

**Source:** Federal Reserve Distributional Financial Accounts

**Tools used:** Python / pandas / matplotlib / Excel

> That is why 2008 mattered so much: the housing crash nearly wiped out bottom-half wealth, while the recovery lifted the financial assets owned mostly by the top.

Your visualization makes it look like the bottom 50% is back to approximately the same share of wealth as pre-2008.

If anything it looks like the compression is among the Top 50% (minus Top sub-10%)

This is fairly misleading on the bottom end, as that 2.5% is not an average of 2.5% of the pie divided by 50% of the population, but most of the bottom 50% being underwater.

It would be more interesting to see the chart start in 1980, pre Reaganonmics.

What are the actual numbers of your cut offs?

This is why its sooo important to be invested. Even if its not much. Just 3% of your savings should be in stocks/mutual funds and not a bank account.

I know people who make little money, never eat out, but they have a 401k or IRA that puts my savings to shame.

„Stocks and businesses“ aka speculative investment and abuse of government contract corruption.

2% minimum tax on all wealth over 100mil

A lot of lower/middle class people just don’t know how to invest or rather actively refuse to do it. They see any sort of risk as an outward scam. Why save anything when you’re already poor? Rather just get immediate gratification anyways. Investing is arguably easier now than any other time in history

I’m confused.

Bottom 50% are all people with less than the median wealth? Ok.

Top 50% are all people with more than the median wealth? Cannot be, otherwise bottom 50+ top 50 should total all wealth.

So what you mean, I think, is brackets as follows:

* Bottom 50

* 50 to 90

* 90 to 99

* 99 to 99.9

* Top 99.9

Edit: would probably be better presented as:

* 50% of population own this

* 40% of population own this

* 9% of population own this

* 0.9% of population own this

* 0.1% of population own this.

Can we see how much $ per group?

> Own assets, or watch the gap widen

Non wealthy have a new tool and they’re using it. Not reproducing is becoming such a popular response to income inequality, even the wealthy are complaining about it. If we can’t balance with money, we’ll balance with population.

How much of this is due to rich people having fewer children

That’s actually fucking astonishing the 0.1% wealthiest haven’t sigmoid’ed their way to owning 99% of all wealth, considering their wealth compounds at the highest achievable rates and other people’s wealth is not invested to the same extent

Could you add in the public debt, divided evenly across the population?

Note also that the 2008 GFC hit black families harder, because it devastated the housing sector and black families statistically had more of their total wealth in their housing than other US racial groups.

Wealth of all households has gone up, but the highest wealth groups have generally gone up more.

How are people with negative net worth handled? If it’s bundled up into the bottom 50% that’s somewhat miss-leading. Also, if anyone runs a across one of these breakdowns that takes life-cycle movements into account I’d be pretty interested (maybe by looking at the breakdown within specific age cohorts?), or alternatively takes into account some notion of human capital and capitalized social security (either full or at the 80% long term sustainable currently funded rate).

To take an extreme example, my sister is a Dr. and her husband is a dentist with an advanced specialty. 15 years ago they had a substantially negative net worth from 100k’s of student loans (and another big slug of debt from buying a house and into a Dental practice partnership/though those should offset net worth wise if properly accounted), but of course that was transitory and together they pull pretty close to 7 figures while living in a moderate cost area and as such their net worth has shot up from the bottom to the 1% tier.

It’s over a longer period of time (I’m older) but I’ve also moved up through multiple of these level and will prob. end up in the 1% tier before retiring from my wife and I both having relatively lucrative careers and modest lifestyle (we’re reasonably close now). I’m not sure how to relate these sorts of charts with those kind of movements which are going to be pretty common in the top 10%-0.5% where lucrative careers (via retirement etc. savings) are the main wealth driver.

The problem with all of these inequality graphs is they fail to account for government transfers. People save less money when they receive more government services. Just looking at percentage numbers like this fails to account for how much changes in saving rates or home prices for most people shifts the graph without any particular change at the top end.

bottom 50 and top 50 do not add up to 100?

After about 2000, it looks like the top 10% is (slightly) more than the top 50% – how is that possible ?

I would add one more reason: age. I would guess that if you computed the average age for each of these subgroups you would find that the wealthier subgroups tend to be older.

How does this compare to other countries?

I’ll bet the 1% taste pretty good.

/shrug

I’m far from top 10% range by net worth but my house is worth (if you trust Zillow and etc) about half of what I have total assets under investment.

It’s also about what you prioritize…I chose the smallest cheapest house in the cheapest neighborhood in my zip code.

This graph needs to be age adjusted and needs some footnoting in regards to how debt is handled. It should also be accompanied by a second graph showing overall wealth improvement not just share of wealth

The 1% could easily lift so many out of poverty but most don’t want to share their wealth because they are heartless bastards.

Congratulations! You are starting down the road of discovery of the Pareto distribution. It’s a mathematical model simplified as the „80-20 rule“ which applies to a huge number of things from wealth distribution to mass distribution of stars.

Most of the mass in stars is accounted for by just a small percentage of stars. Maybe we should have a star mass tax to redistribute it more fairly.

Hey! Over the past few years, my groups share has gotten slightly bigger! Everything’s looking up, finally.

I would like to see this charted back to 1965. I feel like this misses the most dramatic shifts that happened as a result of tax policy changes.

Striking that the top 1% gained share mainly from the rest of the top 50% and not just from the second half