Diese Analyse konzentriert sich nur auf Immobilien, die ursprünglich als verkauft wurden brandneue Häuser und später weiterverkauft auf dem freien Markt. Off-Plan-Käufe sind nicht enthalten.

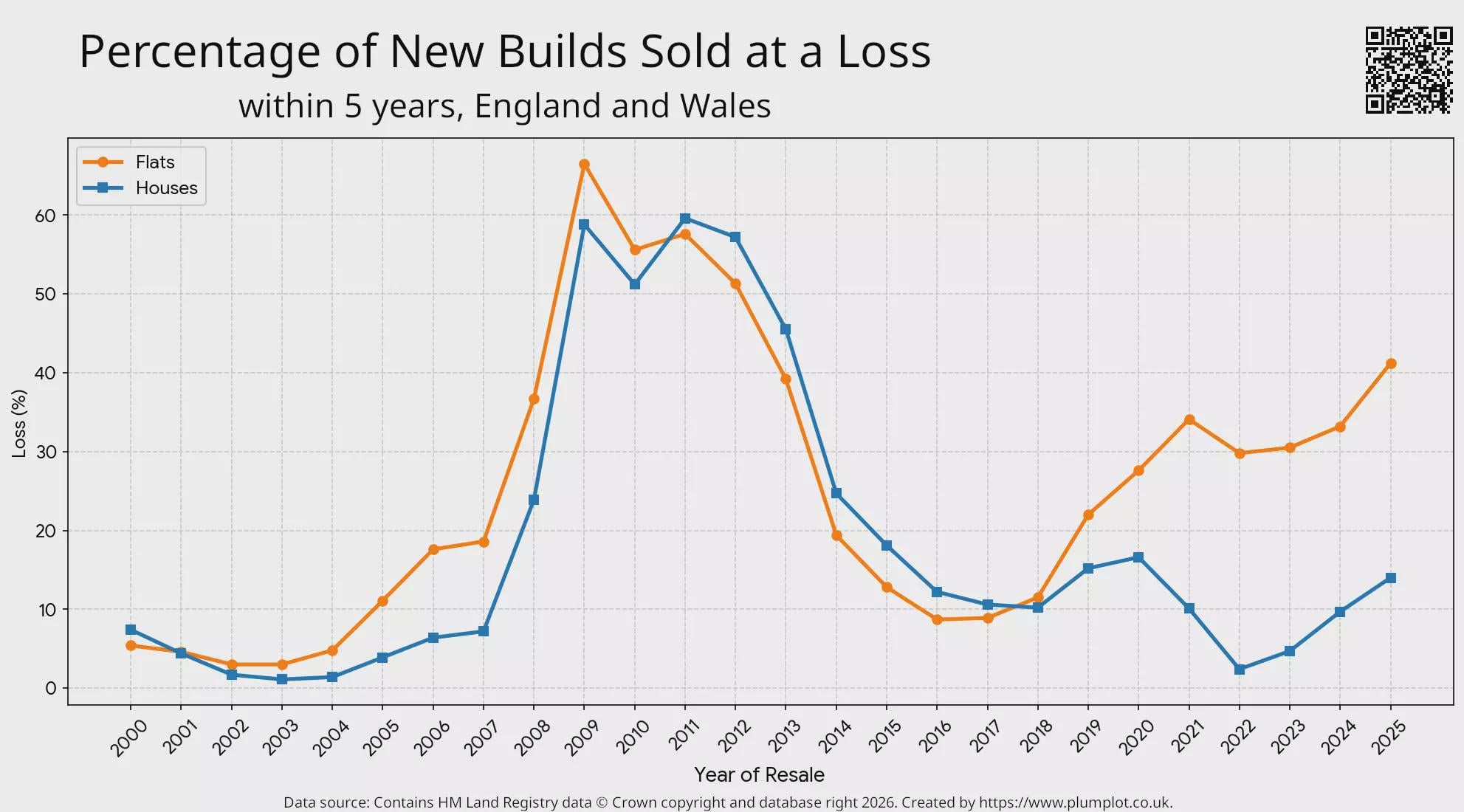

Zum Beispiel im Jahr 2025:

– 41,2 % von Wohnungen Ursprünglich zwischen 2020 und 2024 als Neubauten gekauft, wurden sie für weniger als ihren ursprünglichen Kaufpreis weiterverkauft.

– Für Häuserder Wert lag bei 14 %.

Von vladatb

8 Kommentare

Chart was created with Google Gemini and modified in Gimp.

Data source : [https://www.gov.uk/government/statistical-data-sets/price-paid-data-downloads](https://www.gov.uk/government/statistical-data-sets/price-paid-data-downloads)

License : Contains HM Land Registry data © Crown copyright and database right 2026. This data is licensed under the Open Government Licence v3.0.

More details at [https://www.plumplot.co.uk/posts/losses-on-first-resale-of-new-builds.html](https://www.plumplot.co.uk/posts/losses-on-first-resale-of-new-builds.html)

Presumably this is because service charges on flats have become silly in recent years.

And that’s not even adjusted for inflation

The difference between good and poor maintenance over a five-year period will account for a some of the difference between purchase and sale prices.

I live in Manchester City centre. I love living here. I looked at buying a property and soon realised it wasn’t going to be worth my while. Leasehold apartments sit on the market for ages – if I ever need to sell my property, it would be hard to shift. Service charges are out of your control and can easily spiral. We’ve now decided to move to a house in South Manchester because the risk of a flat in town is too much. It’s sad because I don’t really want to move.

Doesn’t mean the owners actually lost out, if it was cheaper than renting for them, which is possible when interest rates are very low.

It would be really interesting to see this broken down by how much of a loss. Are we seeing an increase in flats sold at say a 2% loss or is it an increases in larger losses? I’m not sure how you’d show it elegantly though.

I think you should also put the non new build houses/ flats on here as a control sample. It’s implied but not shown that new builds are worse. Otherwise this is only really showing us the impact of the financial crash and the recent divergence with flats

These are almost all help to buy sales.

They paid inflated prices at the time because you could buy with only a 5% deposit. E.g. £25000 to buy a 500k house.

People who on the scheme saved 20-40% in mortgage costs for five years. This effect is massive. Even when rates were at say 3%, on a 500k house you’d save £500pm everywhere except London where you’d save £1000pm.

Over 5 years you get the discount for, that’s £28k or £56k in London. That’s on top of the savings you’d make buying a house over renting anyway.

Plus, because the government owns 20%-40% of the value, if you sell for a loss you only take a hit on the remainder. Most people who took this deal have still come out in the money.