Quelle: Federal Reserve Board, G.19 Verbraucherkredit

Werkzeuge: D3.js, gerendert am Measuredworld.com.

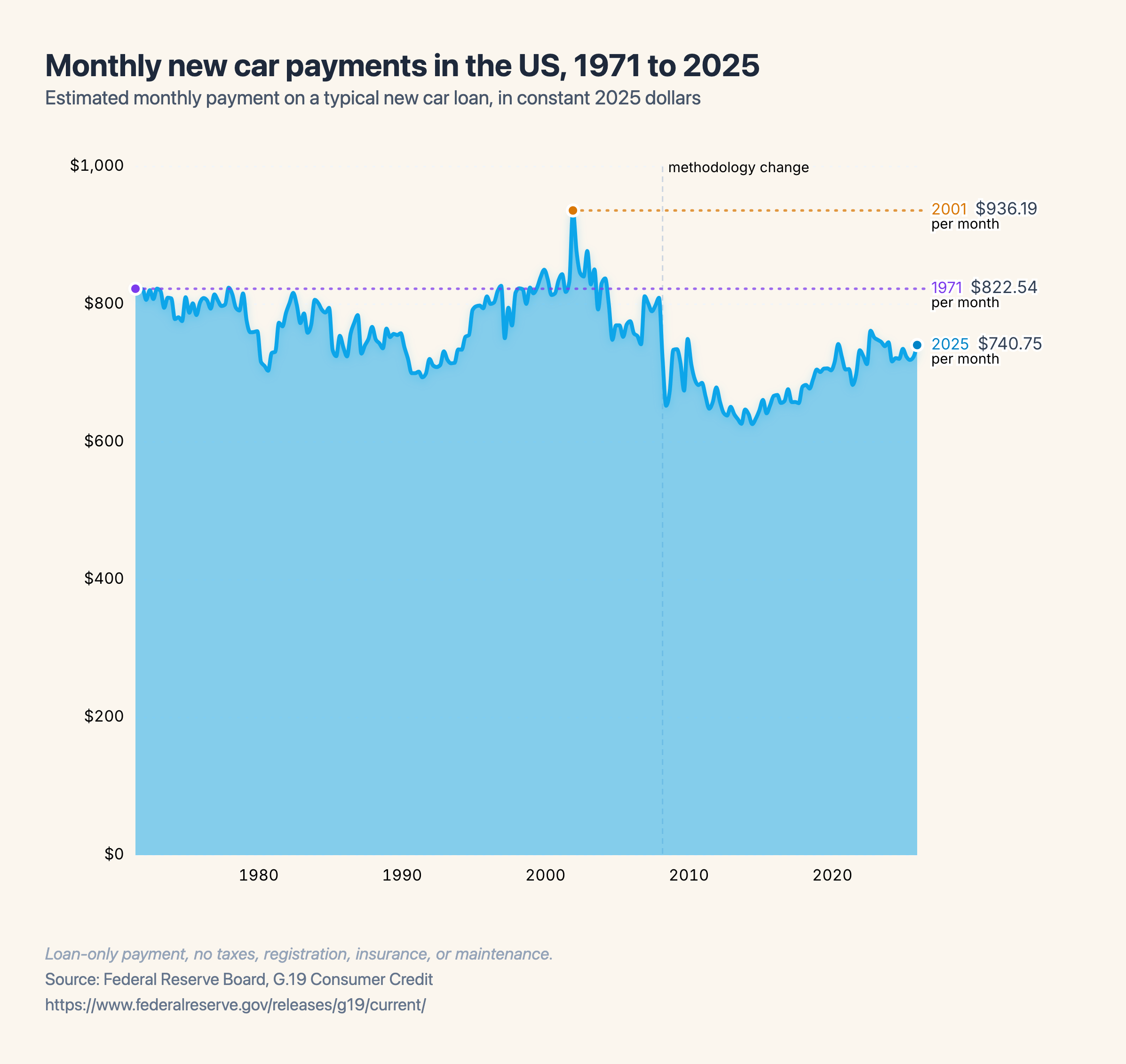

Vorsichtsmaßnahmen: Nur-Kredit-Zahlung. Die Pause 2008 iS eine methodische Änderung in der G.19-Version.

Bearbeiten: Nur um etwas Kontext hinzuzufügen: Heute sind die monatlichen Zahlungen tatsächlich etwa 10 % niedriger als 1971. Selbst wenn die Kredite nur größer wurden, haben die längeren Laufzeiten und niedrigeren Zinssätze dies fast vollständig aufgefangen 72,9 % Erhöhung der realen Kredithöhe. Aber das ändert nichts an der Tatsache, dass die Leute fast doppelt so lange stecken bleiben, bis sie das Geld abbezahlt haben.

Bearbeiten 2: Für alle, die mehr Kontext suchen, wurde ein Betrags-, Tarif- und Laufzeitdiagramm hinzugefügt.

Von Necessary_Cry_5589

20 Kommentare

just 740 a month for 90 months

I bought a car recently. 2016 Honda pilot. 67k. My previous car had its transmission shit on me and at this point in time I couldn’t pay a car payment so I fucked over future me and drained my 401k. Paid cash $20k tags, tax on the road. Same car would had been $430 a month at like 6% interest. It just sucks now.

This chart isn’t doing average people any favors: at first it looks promising, but poor people view debt in terms of payment amount. What actually matters is total amount repaid over the loan duration.

By nature of loan principal being higher, and payment terms being longer, the total cost of financing a vehicle has never been higher. Worse yet, the time between loan pay-off and needing to purchase a new vehicle has also shrunk. Congratulations, viewing depreciating assets in terms of „how much can I afford monthly?“ just flushed an enormous amount of your family’s future wealth right down the shitter!

Dual axis with total paid over the life of the loan would be great. It would show how payments haven’t changed much but total cost of the vehicle has increased due to loan duration.

This just blows my mind. I’m 46 and I’ve never paid more than 419usd/mo for any car I’ve ever owned and I’ve only purchased one used car in my whole life so far. When I see these current car prices and see how many of them are on the road, it blows my mind trying to figure out how people are paying for these things. 80k for a truck and they’re everywhere, 80k used to buy you a house, a nice one. WTF is happening when we’ve normalized these prices instead of rejecting them and leaving dealers with mass quantities of unsold product…

This information is interesting, but also a bit too zoomed out to take anything meaningful from. This doesn’t, for example, do much to show affordability trends of cars or the reasons for those trends. People are able to add context to the graph if they know more, but the amount of context that has to be added is also pretty substantial (to get to “median monthly car costs” you would also have to add insurance, gas/electricity, maintenance, car lifespan, loan length, percent of people who bought a new vs used car, etc).

New car in 1971 are not remotely comparable to new cars in 2025. New cars today have vastly more features then new cars then. A new car in 1971 had:

No airbags

No seat belts

Half the MPG

Less crash resistant

No ABS

No cruise control

No back up camera

No blind spot monitor

No Bluetooth

And the list goes on.

If it was legal to make/sell a new 1971 car today, it would be much cheaper then new cars today.

This is like comparing the price of a bell house phone to an IPhone 16.

now plot months financed and total amoutn paid back

This seems counterintuitive until you realize it’s misleading. People pay far more for cars now, but the monthly payment is the same. You’re just paying for several years longer.

What a deceptive chart. Terrible.

Percentage of income would have been far better measure

Think you should add lines for amount financed in 2025 dollars, average monthly wage in 2025 dollars and average loan duration.

I’ll never understand the people who buy way more car than they can afford. It’s an asset that depreciated rapidly.

My wife and I make over 300k/yr and I cringe at the thought of a car payment over $300/mo or having 2 car payments at the same time. One older car, one newer car, replace the older car once the newer one is paid off.

This is at best misinformation because it’s not corrected for total interest paid.

what was going in in 2001 that there was such a huge spike?

Interest rates were still lower than most of the 1980s

Without time and interest rates, this is basically meaningless.

https://preview.redd.it/ih1gm24wz5zg1.png?width=2394&format=png&auto=webp&s=dcd3cfab71c9a661badbd67c25442c2167ae518d

Here’s a new graph: amount financed (adjusted for inflation), interest rate, and loan term on a typical new car loan in the US.

Ignoring the total cost issue for the moment, these average payments are insane. I am not bad off and I would NEVER consider a loan with payments this high.

I will never understand people who buy new cars with payments like that.

Omg just clicked that’s probably usd too

But paying an extra $500/month to live in the city is too radical