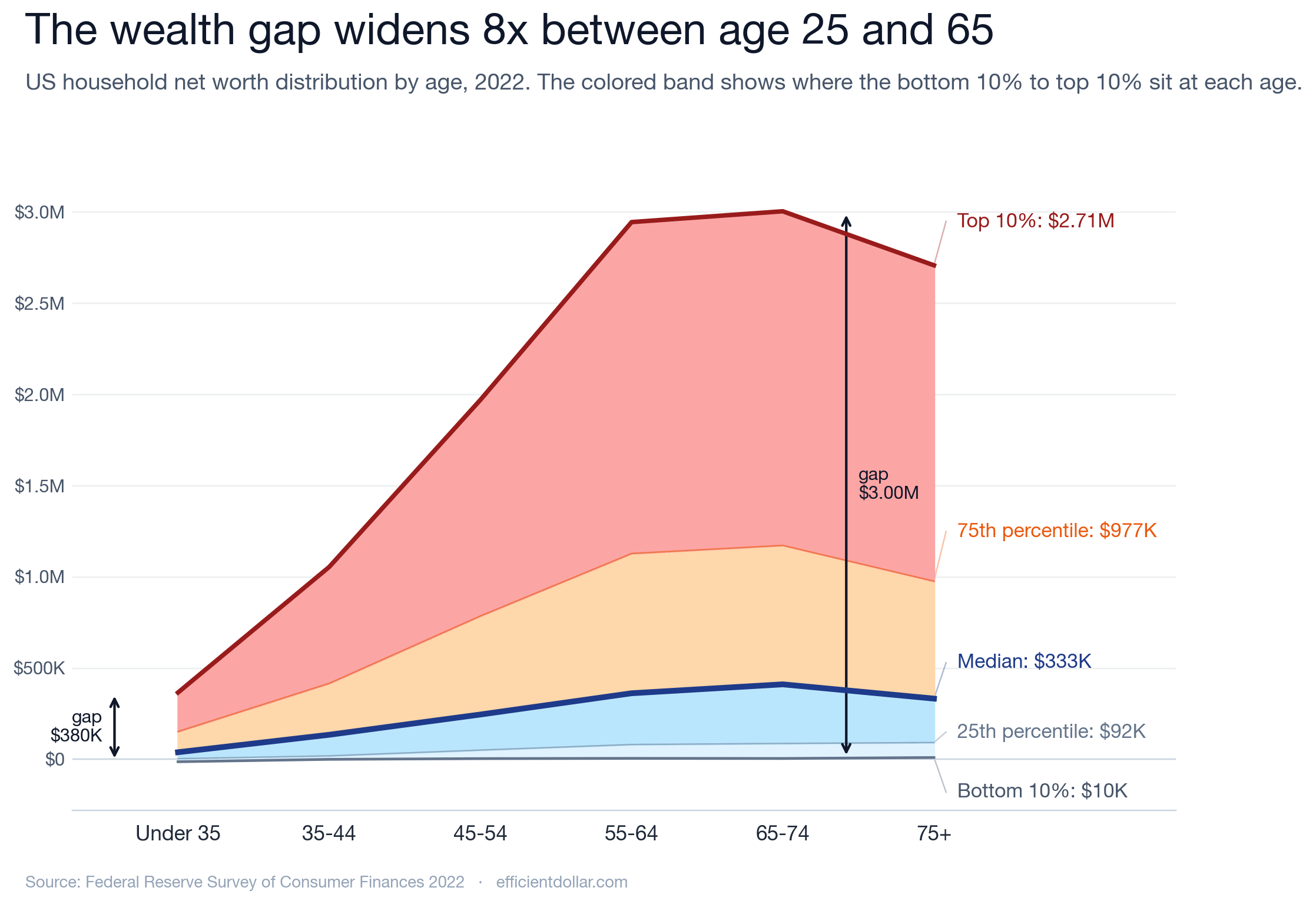

Im Alter von 65 bis 74 Jahren sind es die oberen 10 % der US-Haushalte 3.005.220 $ im Nettovermögen und die unteren 10 % haben 4.896 $.

Der Abstand wächst nicht proportional mit dem Alter. Es erhöht sich fast um das Achtfache von 379.000 US-Dollar (unter 35) auf 3 Millionen US-Dollar (65–74).

Von Global-Thought-1049

31 Kommentare

Source: Federal Reserve [2022 Survey of Consumer Finances]([https://www.federalreserve.gov/econres/scfindex.htm](https://www.federalreserve.gov/econres/scfindex.htm)) (~4,600 households, sample-weighted).

Tools: Python, matplotlib.

Method: For each SCF age cohort, computed the 10th/25th/50th/75th/90th percentile of household net worth (total assets − total debts).

Detailed Methodology: [https://efficientdollar.com/blog/wealth-curve-by-age/](https://efficientdollar.com/blog/wealth-curve-by-age/)

Makes sense, due to compounding growth from investments including home values

I mean, of course. What do you think the wealth gap is at 4?

I know what an age of a person is. But of a household? Is it average of the adults?

Maybe I’m out of the loop, but since when did it become the norm to make an insight the title of a graph? I see it a lot on this sub.

Well yes, when two numbers grow proportionately, so too does the difference between them.

Alternate title: the power of compound interest.

Start early.

The wealth gap between people on the same age group is just how wealthy the wealthiest people are at those ages, because the poorest have nothing at any age.

Its supposed to grow exponentially with age. If you have one person building a retirement fund throughout their life and one person perpetually living paycheck to paycheck, the former will outpace the latter exponentially in wealth, all things being equal.

Its a very clear and informative chart, I just dont agree with the implication I get from your comments.

Imagine being age 65 and not being at least 8x more successful than you were at 25.

Of course it doesn’t grow proportionatly with age. Within each age group, wealth inequality tends to widen over time. Early in life, most people have little accumulated wealth, but differences in income, savings ability, asset ownership, and inheritance lead to divergence. Those able to consistently invest at high rates benefit from compounding returns and the gap widens. Even if wealth couldn’t be inherited the chart would still look like this albeit maybe not as extreme.

No shit. If you save that wealth compounds over time. There’s a group in every generation that blow every dollar they have. And another that never does all that well to begin with. And that gap is always going to be there.

In todays news, water is wet

Well it’s a good thing 65 year olds can easily start families, or this would really impact our birthrate!

This should be presented as a stacked bar chart, no? The lines make it look like continuous data but we have discrete bins on the x-axis

Ugh how do I not have as much wealth as a 65 year old

This makes sense.

If I’m 20 years old and work the same old, stable Union/salary job from age 21-65, my wealth is only going to grow incrementally in that time.

Most wealthy people are entrepreneurs. When they’re 20 years old, they’re probably making less than the person at the Union/salary job. Probably until their 30s, and that’s IF their company/investment takes of, at that point, the wealth gap would sky rocket (up), creating that gap.

So it makes sense that the older people have a larger the wage gap, cause those entrepreneurs have more time to make money at an exponential rate depending on the growth of their company/investment. Whereas the lower middle class and middle class are probably still working the same union/salary job with minimal raises every year to cover inflation, or maybe they have a small business like a restaurant or something that is making ends meet.

It also depends on the spending/saving of each individual as well. Lots of people are paycheck to pay check, sometimes cause they have to be, sometimes cause they’re bad with money. Others save better and that wealth grows when invested in something like the S&P

Either way, it’s logical.

People who vote republican are 1000% to blame.

It seems like the data should exist for each actual age, and not just for age ranges of 10 years.

I mean this chart is just 24 data points, and 16 of those are basically covering 36-74 (with 8 of those data points covering 0-35 and 75+).

The richest infants have comparable lives to the poorest toddlers.

Why does it plateau at 55 to 65? It it nothing more than paying off your mortgage from 30 to 55 then not saving much beyond that?

Most of it is inherited… sadly something some of us will never get to experience

Note the decline at the end. All we need to do is extend human life to 650 (which is when the top 10% meets the bottom 10%) and we will achieve equality.

Human life is extending though (other than current blip) by approx 2.5 years per decade in the US. I’m therefore predicting that we hit equality in the year 25,550.

Data is indeed beautiful, even if life sometimes is not.

Imagine taking the time to build this chart thinking it’s gonna reinforce your flawed views only to just prove that money does indeed compound lmao.

House prices have been rising faster than wages for decades, mostly because of land prices. Land ownership is a zero sum game so those with land become richer and those who don’t become poorer. Wealth is flowing from the young and poor to the older and wealthier.

The biggest determinant of success for young people is the price of their parents‘ home. We are marching ourselves towards a land based inheritocracy.

We need to socialise and redistribute land rents via a land value tax

Older people vote. That explains the graph.

Seems reasonable, a 25 yr old has at most 7yrs of work, 65 has 47yrs. Thats 6.7 times more work, plus add in some inheritance and interest 8, seems good.

A stacked area chart to show something obvious…. Not really r/dataisbeautiful material

Most people start getting promotions and moving up in whatever industry they work in at about 35. By the time they’re 65, they have 30 years of savings socked away. This is surprising to you?

Net worth has exponential distribution so this graph is invalid

This can be explained entirely by time and interest. Assuming the money ($350,000) is in the stock market, which earns ~8% per year, you get **$3,521,929.91**

[https://www.investor.gov/financial-tools-calculators/calculators/compound-interest-calculator](https://www.investor.gov/financial-tools-calculators/calculators/compound-interest-calculator)