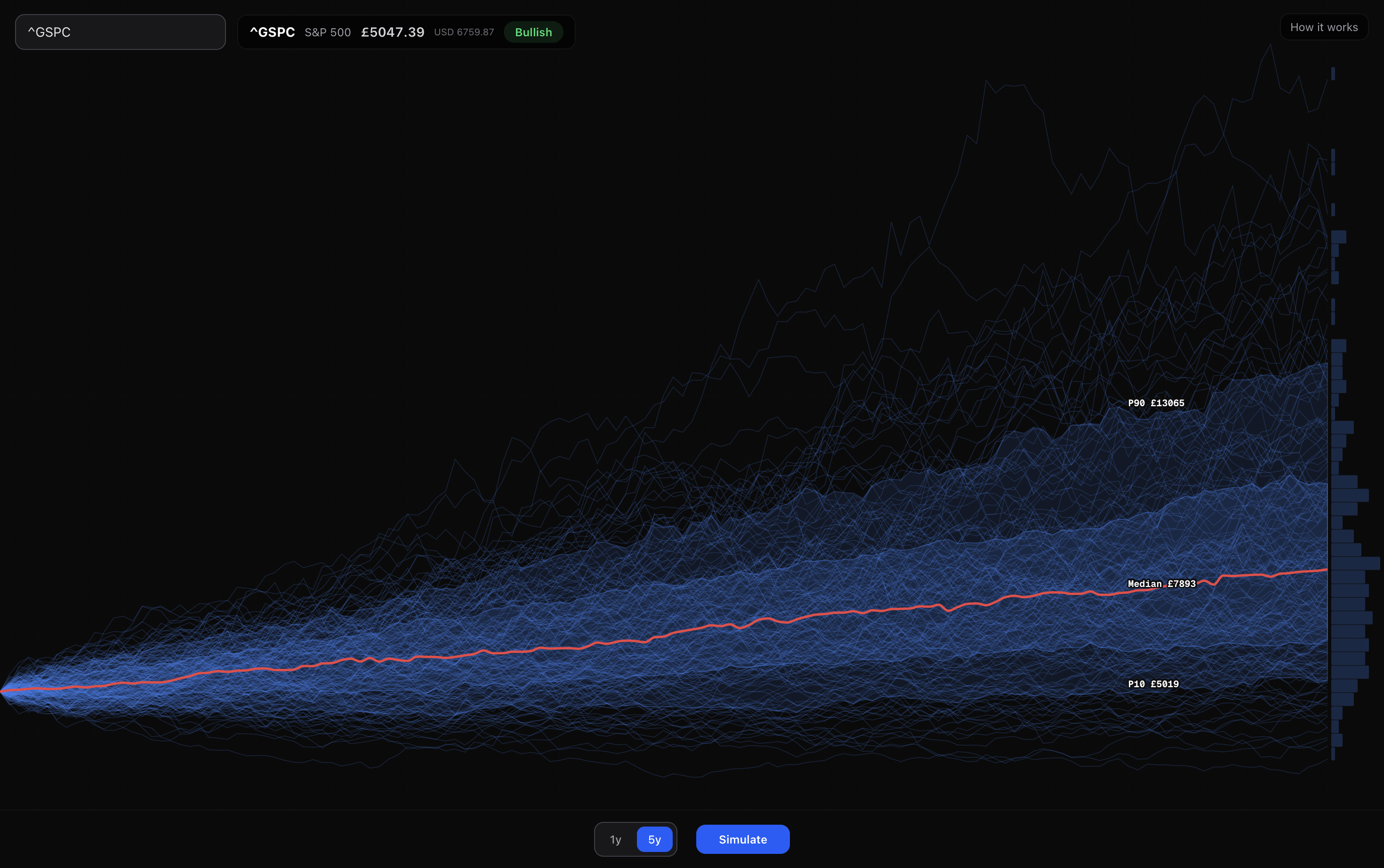

Jede Linie stellt eine mögliche Zukunft für den S&P500 in den nächsten fünf Jahren dar, modelliert mithilfe der geometrischen Brownschen Bewegung mit historischer Volatilität und Drift.

Entwickelt als kostenloses interaktives Tool, damit jeder seine eigenen Simulationen durchführen kann. Lassen Sie einen Ticker fallen, passen Sie die Volatilität und den Zeithorizont an und beobachten Sie, wie sich die Pfade in Echtzeit generieren.

Werkzeug: monte.rorymurray.uk

Gerne beantworten wir Fragen zum GBM-Modell oder der Mathematik dahinter.

Von Both-Hat-1758

7 Kommentare

can i do this too if yes how

https://preview.redd.it/ldijotbx9hng1.png?width=2940&format=png&auto=webp&s=9d3f811c518353db718bd918d3d0431aeb18544f

😍

I thought markets were fat tails distributions

Beautiful visualization. The subtle gradient on the density of the paths makes it so easy to read the probability distribution at a glance.

Always love seeing custom interactive data tools built for the web. I’m working on something in a similar vein for 3D mapping called **HeatGlobe** ([https://heatglobe.com](https://heatglobe.com/)).

What charting library did you use for this, or did you build the visualizer from scratch?

Question: does showing the simulations show anything that just showing the log normal distribution doesn’t?

Have you tried applying this methodology retrospectively and then comparing your results with what actually happened?

Are you using a normal distribution with mean amd standard deviation of daily returns or are you accounting for the skew and kurtosis of the returns by using a Pearson distribution?