Daten: FRED und Yahoo Finance (Gold, Silber, Öl, S&P 500) + FRED (10-jährige Treasury-Rendite)

Werkzeuge: R (ggplot2)

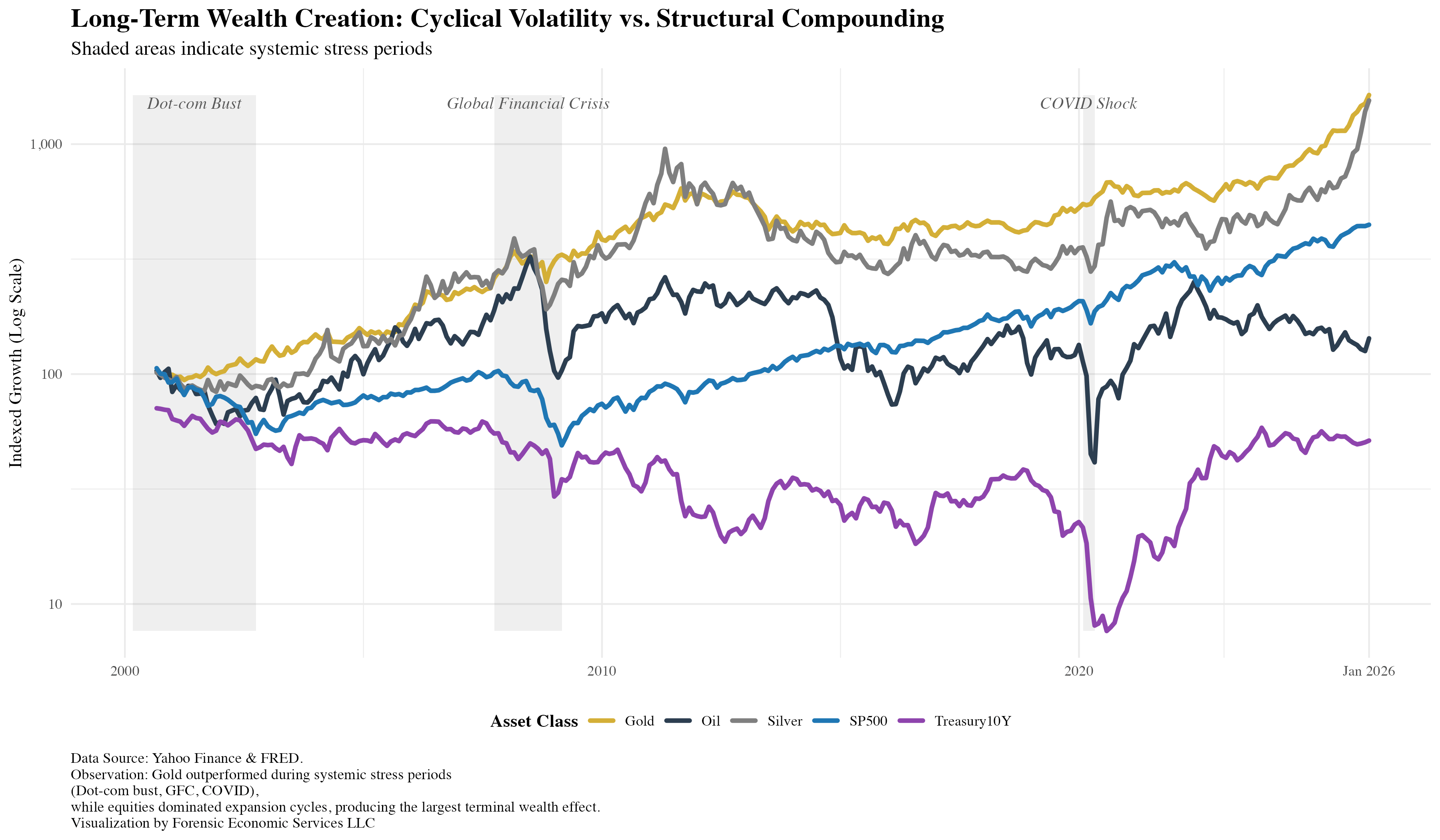

Die Grafik zeigt das indexierte Wachstum der wichtigsten Anlageklassen von 2000 bis 2026, wobei schattierte Regionen systemische Stressphasen markieren (Dotcom-Crash, globale Finanzkrise, COVID-Schock). Logarithmische Skala zum Vergleich der langfristigen Aufzinsung von Vermögenswerten mit unterschiedlichen Volatilitätsniveaus.

Teilen Sie uns Ihre Meinung mit.

Von forensiceconomics

7 Kommentare

Crazy that gold and silver were essentially flat for 10+ years just for them to outperform the S&P500 in the last few years

Why is everything starting at 100, but bonds at ~90?

So… Gold&silver were cheap in the year 2000 and stocks were not…? Is that what you want to show with the graphic?

SP500 line does not include dividends. OP either made a tremendous mistake or is a goldbug looking to deceive.

I know it’s never easy to choose a starting point, but starting S&P 500 tracking just before the .com crash seems a bit of a penalty (and bonus for gold as a safety asset)

Dyno readings for pedal and pop?

This chart is useless – just use a total return index for both bonds and S&P 500. Using a yield scaled to 100 is meaningless and not comparable to the other lines