Ich schaue mir Hypotheken in Polen an und bin ehrlich gesagt schockiert über die Gesamtkosten.

Ich werde dem Beitrag ein Diagramm beifügen, aber die Idee ist einfach:

Wenn ich mir etwas leihe 120.000 € in Polen bei ca 8 %Über die gesamte Laufzeit belaufen sich die gesamten Mehrkosten (Zinsen) auf ungefähre Werte 140.000 €also zahlen Sie am Ende ungefähr 260.000 € in Summe.

In Spanien gilt das Gleiche 120.000 €der Gesamtzins läge näher bei 60.000 € (also insgesamt 180.000 €).

Ich verstehe, dass die Zinssätze je nach Land und Makrobedingungen unterschiedlich sind, aber dieser Unterschied fühlt sich riesig an. Für Leute, die kürzlich in Polen gekauft haben:

Ist das im wirklichen Leben tatsächlich so, oder übersehe ich etwas (Gebühren, feste oder variable Gebühren, Laufzeitannahmen, vorzeitige Rückzahlungen, Neuverhandlungen usw.)?

Wenn Sie in Polen sind: Welchen Tarif haben Sie erhalten, fest/variabel, und in welchem Jahr haben Sie den Vertrag unterzeichnet? Gibt es Tipps zur Vermeidung von Überzahlungen (z. B. Refinanzierungsstrategien, kürzere Laufzeit, höhere Anzahlung)?

(Ich poste hauptsächlich, um zu verstehen, was hier „normal“ ist und was nur die Worst-Case-Rechnung des Taschenrechners ist.)

https://i.redd.it/aq9edrm8uj9g1.png

Von Professional-Tax3077

30 Kommentare

One of the reasons is flipping, and flippers people.

!remind me 1 day

This is unfortunately normal, but you’re forgetting to factor in the currency difference. In Poland, PLN has a higher inflation rate than the EUR. Factoring in the inflation difference you’ll come up with a similar (still worse in Poland, just similar) end value after paying it off. Ideally, overpaying monthly will significantly reduce the final interest cost.

Poland has higher inflation and a much much faster growing economy than Spain as you brought up. That usually means higher mortgage rates

>Is this normal?

Yes.

https://preview.redd.it/tb2by56gyj9g1.jpeg?width=921&format=pjpg&auto=webp&s=b0c29f491dcd0f13a60f22fb215d35c6d02bf7c0

!remind me 2 day

Welcome to Rzeczpospolita-Ketchupowo-Deweloperska. We have biggest credit costs and most expensive m2 compared to wage in Europe.

Ofc problem is more complex, one is that flats/houses are considered as investment for majority of janusz of buisness, since they are not clever enough to invest in stock market. Others are banks. Banks are having time of their lives in case of income in Poland grossing and beating records each year, despite that we have highest credit costs, worse standards of credits or bank account costs. Another is poor level of debate about cadastral tax, where people dumb try to convice people it’s not needed since elders who barely can buy drugs and food will lose on taxation from 3rd property. This is also one of many factors of declaining demography.

We just let banks scam everyone. the economy is not the reason for it. banks simply realised they have a monopoly and can charge high interest, and people will still go in debt.

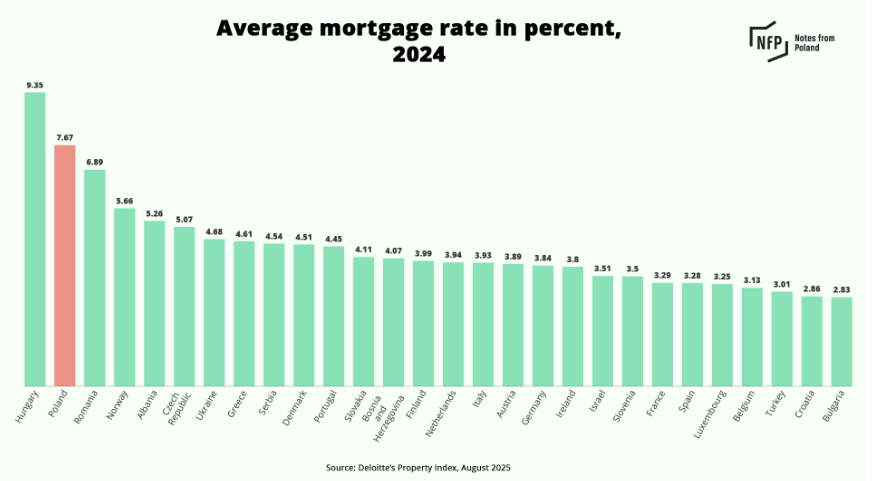

I’m more confused by how Turkey has the 3rd lowest mortgage rate with a 38% interest rate

https://preview.redd.it/fpbte5za0k9g1.png?width=776&format=png&auto=webp&s=838dd595ef0a699efb58abb80a669306282f613e

It is normal because Poland have own currency. For the last 20 years Spain salary in eur increase on 50%, in Poland in 4 times

That’s probably the last thing that stops apartment prices from going totally insane. Housing market in Poland is already totally sick, because it is absolutely detached from peoples income. To solve this we have to limit loans so the prices must be more rational or you would not sell it at all. Currently developers can give us literally any price, and still there will be someone to pay – 30 years loan instead of 20 years, what is the difference? You will always find someone more desperate.

Hopefully in december 2025 it’s 6% not 7.5%

In Poland most mortages are related to POLISH interest rate, which is higher than EUR or USD. PLN has higher rate. Inflation is sub 2,5% so below target, but interest rate is like 4%.

It is tense topic, since there is a space for lowering it more, but also polish monetary economist have stick in ass in general, since in 90s there was mass inflation period, so they are always safe player, extra safe to the level of deflation.

Which is probably bad, since with lower rates poland could get some extra jobs.

There is extra layer, as there are bank taxes on volume of borrings, which could work similar to extra interest rate. Polish Bank sector quite competitive (many banks) and some are national (state owned), so they are not particulary greedy (but a little yes).

This isn’t normal, or at least shouldn’t be…

I took a loan in Slovakian bank.

I hope that our currency won’t crash in the next 5-7 years, so I can repay my mortgage.

It’s so much cheaper in euro.

I am going to take morgage with 5.7% where you see 8%?

Join the eurozone -> lower interest rates -> lower costs -> lower mortgage costs. But the poor do never understand and the populists feed this dumbness.

Welcome to capitalism

Yes, it’s normal. They fighting hard against ownership in Poland. You will own nothing and they will be happy.

Sadly yes. Our country ir runing by banksters.

Because we are rich and we want to pay more.

Rate is normal.

People still expect to purchase prime location in the city center and pay what their parents did who earned x5 less than they are earning.

Until the mentality will not change and there will be an outflow into suburbs the Insanity will continue.

This is the result of the policies made by far right populists

Thank you for your research,

Now check what’s central bank and who sets reference rates. Then cry

That’s the reason why apartments are significantly cheaper in Poland in same size cities near borders with Slovakia.

Yes we like to pay more

https://preview.redd.it/fd870lqs4k9g1.jpeg?width=1334&format=pjpg&auto=webp&s=4b8614edf49db87aa6c3df4c676a22e5f29f5b0b

1. The % will drop, for now you can get around 6%, it is becouse of previous inflation, no way it will stay at 8% for long.

2. You can actually pay more that mortgage every month, that will decrease the anmount to pay

I got a 250k mortgage last year in Estonia. 1.35% bank margin + EURIBOR.

No ale jakie PKB mamy.