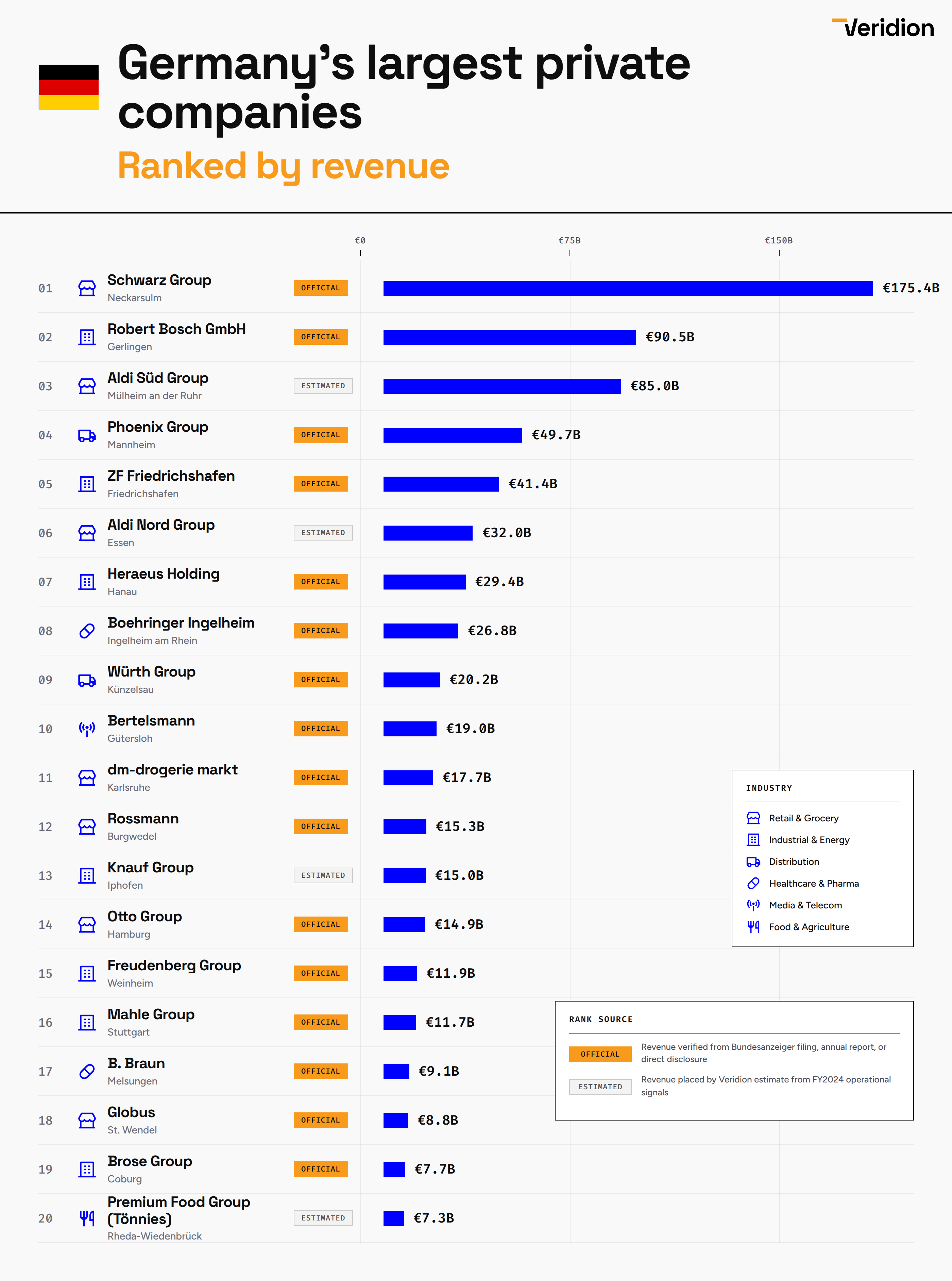

Data: Veridion company intelligence + Bundesanzeiger filings + news/press signals + industry benchmarking. Tools: Python, React + SVG, Remixicon, Claude.

Data on Germany’s largest private companies is scattered across Bundesanzeiger filings, group press releases, and trade press, and rarely pulled into one ranking. This is built on Veridion company intelligence, cross-checked against group annual reports and direct disclosures. For companies that don’t publish consolidated revenue (Aldi Süd, Aldi Nord, Knauf, Premium Food Group), we run an inference model on operational signals: product catalog, subsidiary filings, employee count, geographic footprint, physical locations, and industry benchmarks. OFFICIAL = verified from a filing or disclosure. ESTIMATED = Veridion estimate from FY2024 operational signals.

Exclusion rules: no public shares, no >50% foreign ownership, no cooperatives, no mutuals, no foreign partnerships, no state-owned. That cuts Edeka and REWE (cooperatives, ~€75B and ~€95B), Liebherr (HQ Switzerland), Theo Müller (Luxembourg), Linde (Ireland), Mars Deutschland (US-owned), Deutsche Bahn (state-owned), and the global Big Four partnerships. Foundation-owned Bosch, Bertelsmann, Mahle, and ZF qualify since they have no public shares. Rossmann is 60% family / 40% A.S. Watson, so family majority keeps it in. Heraeus revenue includes precious-metals trading volume per group reporting.

„Schwarz is known to be very protective of his privacy, to an extent that no media recordings of Schwarz exist, and he refuses any kind of interview. Meanwhile, just three photos of him are known to exist in the press or in the image search of Google“

that’s crazy

nosocksinside on

What about Merck Group, they are a private company.

TheBlacktom on

What year is this data from? Can you maybe show trends, changes over the years? Compared to 5 years ago, 10 years ago, etc?

wreck0 on

TIL Aldi owns Trader Joe’s but a different Aldi than Aldi.

cLax0n on

Am I being semantic if I say that inferring a company’s size based on revenue is wrong? I feel like asset size is the more useful metric for that. Not even net assets size, just raw asset size.

Bosch generates billions in revenue through large scale industrial manufacturing, long term business contracts, automotive technology, global sales, and continuous innovation…

123Flop456 on

What about Rethmann group. 24.5B revenue in 2024 and no public shares.

AggroJordan on

ZF highly ranked but struggling to stay relevant at all though…

Auspectress on

Largest Polish company is 7 bil € so we almosy catched up with Germany

IMMoond on

Fun game for this list: look up the places where these companies are headquartered on Google Maps. Like half of them are in a small town in bumfuck nowhere. It’s a quirk in Germany, these companies come out of nowhere and then stick around there because they’re still privately held

Leave A Reply

Du musst angemeldet sein, um einen Kommentar abzugeben.

13 Kommentare

Full dataset: [https://docs.google.com/spreadsheets/d/1jQsvHW9Th8YS0JXG2_uDIuyMeYGrwu6dwNlcTkpGeN4/edit?usp=sharing](https://docs.google.com/spreadsheets/d/1jQsvHW9Th8YS0JXG2_uDIuyMeYGrwu6dwNlcTkpGeN4/edit?usp=sharing)

Data: Veridion company intelligence + Bundesanzeiger filings + news/press signals + industry benchmarking. Tools: Python, React + SVG, Remixicon, Claude.

Data on Germany’s largest private companies is scattered across Bundesanzeiger filings, group press releases, and trade press, and rarely pulled into one ranking. This is built on Veridion company intelligence, cross-checked against group annual reports and direct disclosures. For companies that don’t publish consolidated revenue (Aldi Süd, Aldi Nord, Knauf, Premium Food Group), we run an inference model on operational signals: product catalog, subsidiary filings, employee count, geographic footprint, physical locations, and industry benchmarks. OFFICIAL = verified from a filing or disclosure. ESTIMATED = Veridion estimate from FY2024 operational signals.

Exclusion rules: no public shares, no >50% foreign ownership, no cooperatives, no mutuals, no foreign partnerships, no state-owned. That cuts Edeka and REWE (cooperatives, ~€75B and ~€95B), Liebherr (HQ Switzerland), Theo Müller (Luxembourg), Linde (Ireland), Mars Deutschland (US-owned), Deutsche Bahn (state-owned), and the global Big Four partnerships. Foundation-owned Bosch, Bertelsmann, Mahle, and ZF qualify since they have no public shares. Rossmann is 60% family / 40% A.S. Watson, so family majority keeps it in. Heraeus revenue includes precious-metals trading volume per group reporting.

https://boingboing.net/2026/04/21/bosch-buys-bosch-from-bosch-and-bosch.html/amp

„Schwarz is known to be very protective of his privacy, to an extent that no media recordings of Schwarz exist, and he refuses any kind of interview. Meanwhile, just three photos of him are known to exist in the press or in the image search of Google“

that’s crazy

What about Merck Group, they are a private company.

What year is this data from? Can you maybe show trends, changes over the years? Compared to 5 years ago, 10 years ago, etc?

TIL Aldi owns Trader Joe’s but a different Aldi than Aldi.

Am I being semantic if I say that inferring a company’s size based on revenue is wrong? I feel like asset size is the more useful metric for that. Not even net assets size, just raw asset size.

[https://de.wikipedia.org/wiki/Cordes_und_Graefe](https://de.wikipedia.org/wiki/Cordes_und_Graefe)

Bosch generates billions in revenue through large scale industrial manufacturing, long term business contracts, automotive technology, global sales, and continuous innovation…

What about Rethmann group. 24.5B revenue in 2024 and no public shares.

ZF highly ranked but struggling to stay relevant at all though…

Largest Polish company is 7 bil € so we almosy catched up with Germany

Fun game for this list: look up the places where these companies are headquartered on Google Maps. Like half of them are in a small town in bumfuck nowhere. It’s a quirk in Germany, these companies come out of nowhere and then stick around there because they’re still privately held