Datenquellen:

- FRED (Wirtschaftsdaten der Federal Reserve)

- US-Volkszählungsamt

Visualisierung: R (ggplot2)

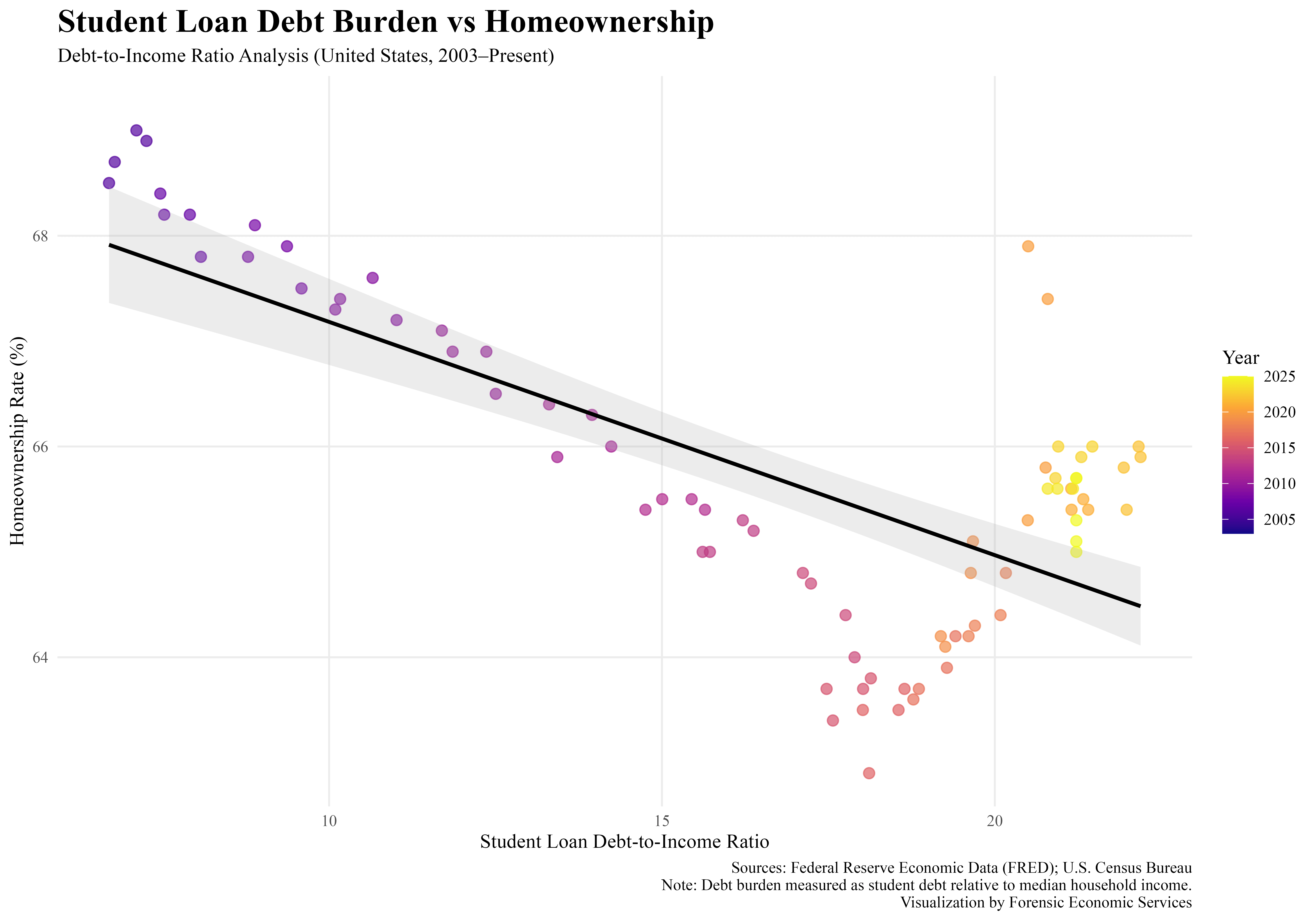

Hält die steigende Verschuldung der Studenten den Eigenheimbesitz zurück?

In dieser Grafik ist das Verhältnis von Schulden zu Einkommen für Studiendarlehen im Vergleich zur Wohneigentumsquote in den USA im Zeitverlauf dargestellt. Jeder Punkt stellt ein Jahr von 2003 bis 2025 dar, wobei die Farbe den zeitlichen Verlauf anzeigt.

Es besteht ein klarer negativer Zusammenhang: Als die Schuldenlast der Studierenden zunahm, sanken die Wohneigentumsquoten im Allgemeinen – insbesondere in den 2010er Jahren. In jüngerer Zeit hat sich der Anteil des Wohneigentums teilweise erholt, auch wenn die Verschuldung weiterhin hoch ist.

Dies deutet darauf hin, dass es möglicherweise Studentenschulden gibt ein Stück des Puzzles – aber nicht die ganze Geschichte. Auch das Wohnungsangebot, die Zinssätze und die Demografie spielen wahrscheinlich eine wichtige Rolle.

Wir freuen uns auf Ihr Feedback.

Das Team von Forensic Economic Services LLC | Rule703.com

Von forensiceconomics

10 Kommentare

Why are the Trump Republicans so against helping out with student loan debt?

there are way more than 20-something data points here

is this quarterly?

neat how debt to income ratio also appears to be strongly correlated to year

Funny how the X axis effectively shows elapsed time

Could this be explained by the age distribution of people in the US? Birthrates peaked in the 2000s so it makes sense there’d be a spike in student loans now that all those people are in college or recently graduated.

This is an interesting chart, but also a somewhat confusing one, at least to me. Using the color is an elegant way to show progress over time while still showing both D/I and the ownership rate, but it leaves me unsure on what’s happening at the end, where it seems like there’s a sharp change in a particular year, but it’s not clear what year exactly the shift occurs—something that I am doubly unsure about because the averaging line seems to suggest a much more straight forward drop as D/I gets higher.

This is a really good example that correlation != causation. While payments for student loans may be holding back homeownership the massive increase in home cost probably plays a larger role.

However, the shift from low-cost subsidized tuition AND home prices exploding both occurred at the same time.

I think this is a very simple graph to show some form of correlation; however, it’s more complex than simply saying the more student loan debt one has lowers the probability of home ownership. For example, government spending and QE have more weight to home ownership than student loan debt. Stagnant wages with increased inflation has caused people with student loans not to have home ownership. Any sort of massive debt has an impact on home ownership such as credit card debt or auto loans being the next big one.

Ironically my high debt-to-income ratio helped me buy my first home. Qualified me for a state-sponsored first-time home buyer credit which helped with the down payment.

Why linear regression for non linear data?