Quelle: Eurostat.

Methodik:

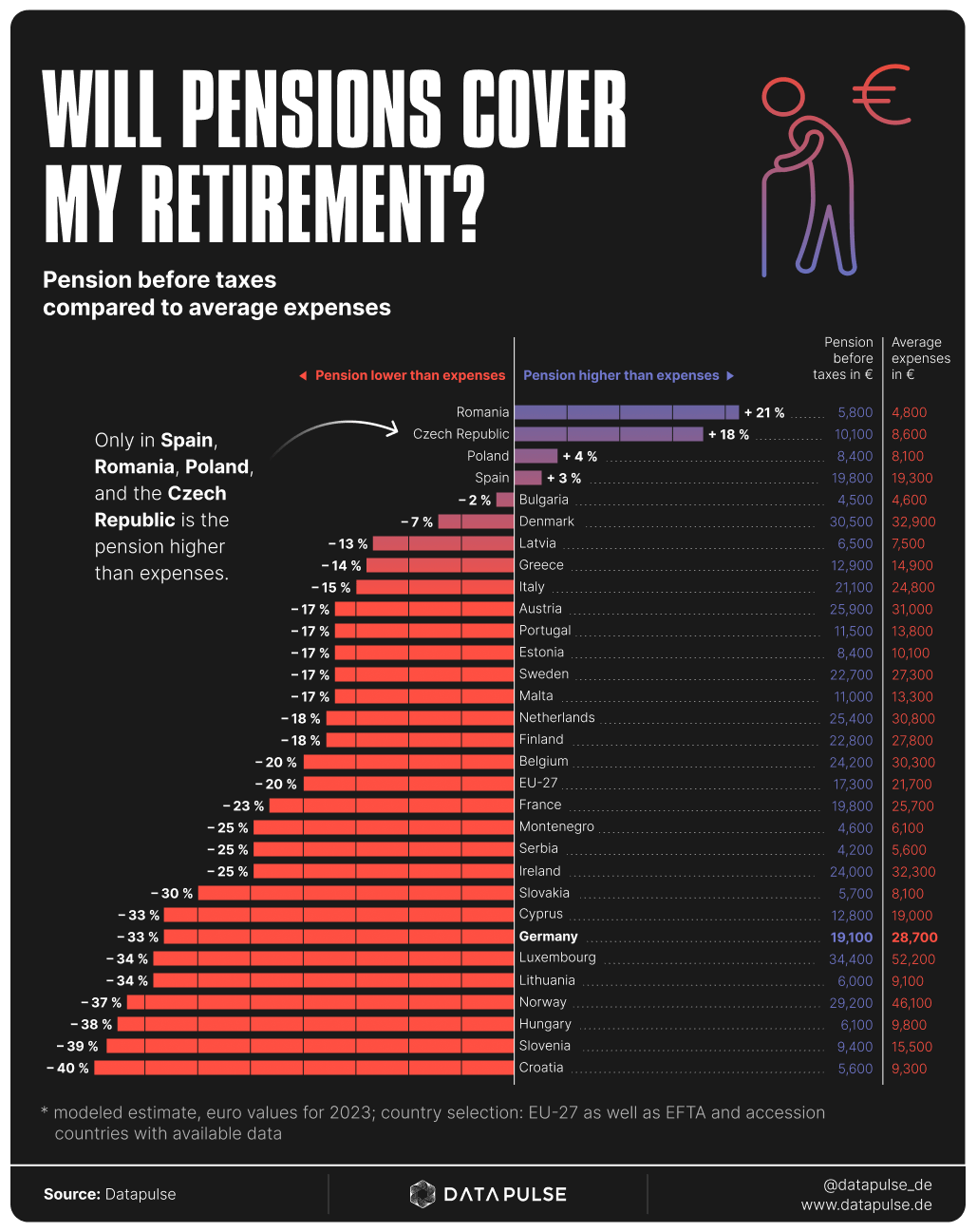

Dies ist eine modellierte Vergleichsanalyse. Die durchschnittlichen staatlichen Bruttorenten wurden mit den geschätzten durchschnittlichen jährlichen Ausgaben von Personen ab 60 Jahren verglichen. Die Ausgabenwerte wurden länderübergreifend harmonisiert und die Inflation an das Preisniveau von 2023 angepasst, um einen länderübergreifenden Vergleich zu ermöglichen. Die Ergebnisse werden als prozentualer Überschuss oder Defizit der Renteneinnahmen im Verhältnis zu den Ausgaben ausgedrückt.

Werkzeuge: Datenextraktion von Eurostat. In Python durchgeführte Analyse. In Figma entworfene Visualisierung.

Wichtige Erkenntnis:

In allen außer vier Ländern deckt die durchschnittliche staatliche Rente die durchschnittlichen Ruhestandskosten nicht vollständig ab. In einem großen Teil Europas beträgt der Mangel mehr als 20 Prozent.

Von DataPulse-Research

23 Kommentare

Average US citizen: “What’s a pension?”

EU-27?

And is it still not worth keeping the UK in charts like this?

**public** pension being the key word here.

Pretty misleading chart. I mean, in the Netherlands you would only get just the state pension if you never worked a day in your life. Probably the same all around Europe.

The data might be accurate, but it is not representative of the average person.

Where do these average expenses come from? Seem incredibly low. I’m assuming they’re distorted by the people that own property outright, which would dramatically underrate the expenses for those that don’t

Are these pensions for former government workers? Or are the generally for all citizens?

If tax protected retirement accounts that you could invest in were more commonly allowed in European countries you wouldn’t need government aid in retirement

In Denmark you also have to work until 70+, cant be compared with other countries where age of retirement is somehting like 64.

At least for the highlighted row the state pension was never claimed, marketed or intended to be one-stop age insurance. You were always expected to complement it with private savings and/or company pensions.

As another data point, my US public pension (teacher in California) will be at least €83,500/year, depending on how long I keep teaching.

Edit: Yearly expenses are around €50k.

There’s another angle to this – you can retire so much earlier in Europe. I think in Greece, you can retire at 55.

I’m Romanian-American and most of my relatives live in Romania. This chart isn’t really the flex people think it is.

The Romanian pension system is a mess that is currently threatening to bankrupt the entire country. The reason it’s so high is because it was used for years as a way to legally buy votes: “vote us in and we’ll raise your pensions”. Even the party in power would often preemptively raise pensions as an election approached, even if they lost after. This happened in 2024.

Pensions increased pretty much every election cycle, and they are now completely unsustainable

Now, the few honest people in government are trying to reform the system but political factions and the Supreme Court (known for its own corruptions) are fighting it.

Edit: I should have also mentioned that certain pensions serve as a form of bribery/corruption. The infamous “judicial pensions” for judges and prosecutors are almost 10x the typical pension for a Romanian, with some being higher than $70,000 a year, in a country where the median person makes $22,000 a year! The retirement age for judges and prosecutors is laughably low at only 50, so they‘ll often have more time on the fat pension than actually working.

Imagine if in the US, judges and prosecutors could retire after 20 years of working, then collect $200,000 yearly in government checks for the rest of their lives.

You’ll never guess what the judges think about the “constitutionality” of reforming these pensions…

Average expenses aren’t remotely close to acurate for Spain, especially the populated areas. Just the rent or mortgage easily pushes expenses over 10k.

Average expenses in this case is really misleading. These averages often include things like rent or mortgages, which old people for the most part don’t have to worry about. Then there’s expenses on children that old people again don’t have to worry about.

I’m surprised that France isn’t higher, I often see French on the internet claiming that pensioners are able to save more than working French.

Kind of a backwards way to look at the data.

Expenses <= pension + savings / expected lifetime

So it is really more like ‚average retiree has saving and/or supplemental non-state pension.‘

What this probably doesn’t account for is other social programs that people may be getting help from. For example, in France, someone earning below a certain amount can apply for public housing that has a greatly reduced rent. Healthcare costs are also covered for the most part.

Do I even want to see what the US’s looks like?

The average pension would only equal the average expense in a world where no retirees had saved any money other than their pension. This is a classic misleading analysis similar to when people compare minimum wages to average expenses. Of course average expenses are going to be higher than minimum wages, if they weren’t there would be people making above minimum wages and choosing not to spend that money.

Think of it like this if 10 people got a $100 pension and had no other savings and 10 people saved some cash before retiring and used it to spend an extra $20 per week this analysis would show that the pension in our fake country didn’t cover retirement costs.

The analysis also includes people 60 and older, while the average retirement age in most of these countries is 65. So the higher expenses of employed individuals are also being thrown in to make the data look worse.

The last point is probably the reason that Romania, Czech republic, Poland and Spain look so good. They have really generous pension systems and really really bad labor markets. So if you’re a 60 year old, your wages are really low which pulls down the spending, and you’d essentially get a raise when you retire. Generally speaking that’s really bad policy.

Is any pension fund not funded by massive oil revenues actually funded?

Edit: added any

Ah, noted. Retire in Romania, Czech Republic, Poland, or Spain.

So, a German could just take their pension and invade Poland, as is tradition.

Bulgarian pension 4500 euro? Is this per annum?