Hallo zusammen, ich bin EU -Bürger und arbeite seit einigen Jahren glücklich in Finnland. Ich bin ein qualifizierter und spezialisierter Arbeiter mit einem Karriereweg, der als sehr gutes Gut für die finnische Firma angesehen wird, für die ich arbeite, die ich liebe und wo ich wirklich viel gedeiht. Ich habe hier lokale Freunde und halte mich für glücklich, ich habe beschlossen, langfristige Pläne für Finnland zu haben. Eine gute Zusammenfassung von all dem kann sein: Ich lebe in Finnland, weil ich es will, nicht weil ich muss. Finnland ist ein Ort, den ich liebe und zu dem ich beitragen möchte.

Neben dem Denken in einem Land kommt auch die Verwaltung persönlicher Finanzen: Ich habe einen Investitionsplan, der mir hilft, mein Altersvorsorgeeinkommen aufzubauen und die Inflation zu entsprechen. Ich bin der Meinung, dass dies (auch bekannt als AKA "Ersparnisse"Anwesend "langfristige Investition") ist nichts exklusiv "reiche Leute"eher etwas, was jemand haben sollte und mit all dem kostenlosen Wissen, das wir heute online haben, zugänglich sein sollte. Kurz gesagt, etwas, das einen größeren Teil der Staatsbürgerschaft zugute kommt, nicht nur "die wenigen".

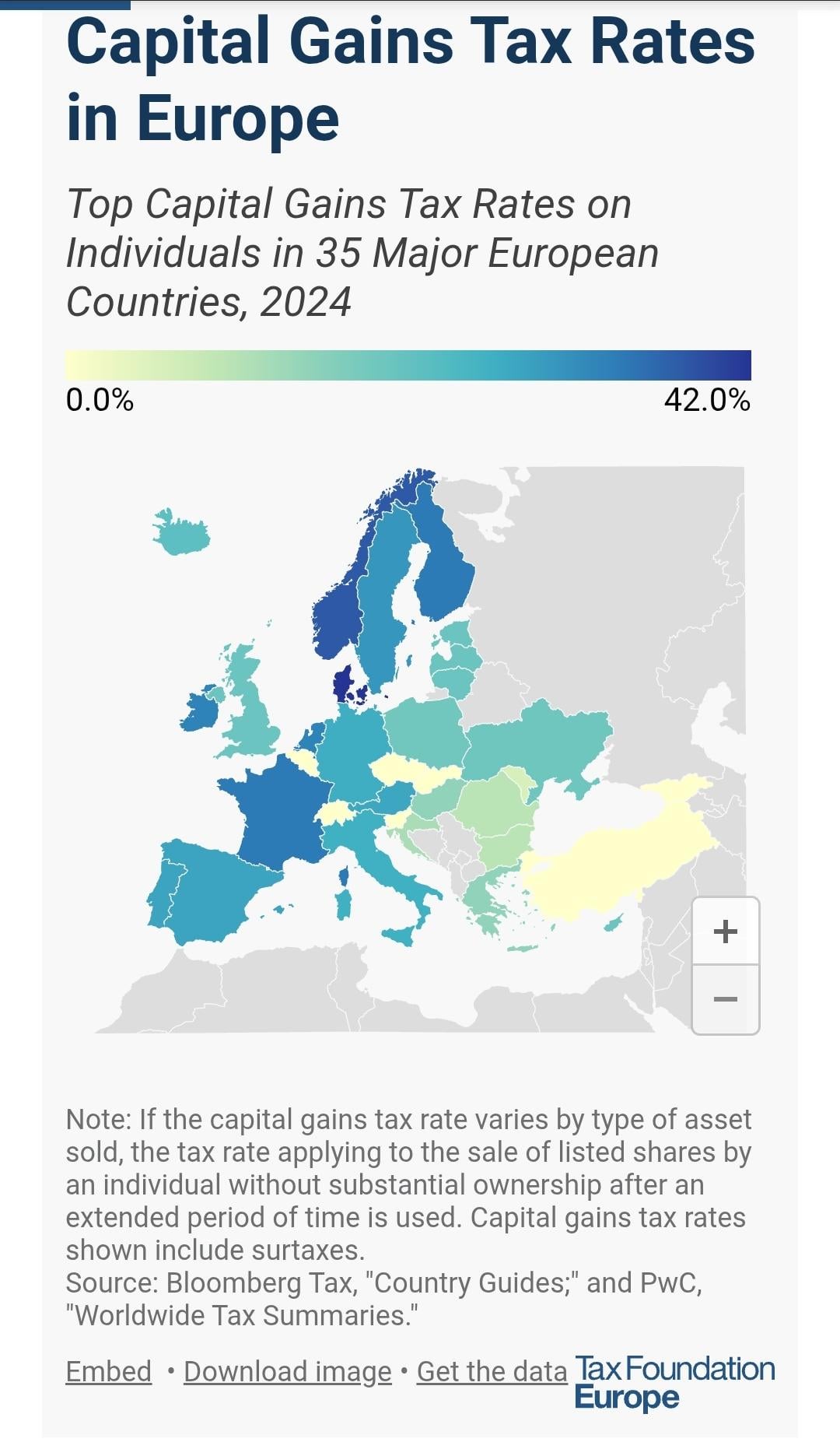

Aber jetzt stelle ich fest, dass, wenn ich mein ganzes Leben lang in Finnland bleiben würde, nach harter Arbeit und Ersparnis, mehr als ein Drittel (34%) meiner Ersparnisse als Person der Mittelklasse von der Regierungswesen weggelöscht werden. Die Steuer gehört zu den höchsten in Europa und kürzt sehr flach, unabhängig davon, ob es sich um einen anderen Vermögen/Hintergrund einer Person handelt (siehe Link unten für andere Möglichkeiten für die CGT-Anmeldung) 1). Diese Maßnahme fördert es nicht und angesichts der aktuellen Aussichten zur Zukunft des Ruhestands ist dies nicht ratsam aus dem Staat. 2) Ich verstehe "Die Reichen besteuern" Aber diese Steuer trifft sehr generell jeden, auch diejenigen, die keine Millionen als Sicherheitsnetz haben.

TL; DR: Langfristig (30 Jahre) kann sich ändern, die Politik kann variieren, Gesetze können erfolgt. Daher ist meine Frage: Wie wurde die CGT in Finnland bisher wahrgenommen? Ist es jemals in der Vergangenheit in den Diskussionen über Reformen gewesen? Hat es ein Politiker jemals angesprochen? Könnte es in der Zukunft oder in der Zukunft angesprochen werden, weil sich die Mehrheit der Wähler auf die eine oder andere Weise nicht beeinflusst/davon profitiert? Würde es eine große Abstimmungsbasis dafür geben?

Und natürlich freuen Sie sich, all Ihre Kommentare und persönlichen Erfahrungen darüber zu hören.

Danke! (Bildquelle https://taxfoundation.org/data/all/eu/capital-wainains-tax-rates-in-europe-2024/ )

https://i.redd.it/75gz80jsy5hf1.jpeg

Von _knope2020

7 Kommentare

Only gains I have are around my waist. Pls don’t tax that.

Classic tax punishing the masses to benefit the rich. Yet nobody talks about it cos there is this idea that only the wealthy pay capital gains…

Should be changed, but most likely won’t. Would be good to have at least a more attractive option for gains on long term investments…

„Over one third of your savings“ isn’t quite correct: you pay 30% up to 30 kEUR of capital gains, and 34% only on anything on top of that. And of course you only pay for the capital gain portion of the securities you sell.

I’d also be mindful of the alternative taxation scheme which you are allowed to use, the *deemed acquisition cost,* which is perhaps underappreciated because it can make a big difference. Especially for securities held for a long time and with a lot of capital gains, it can push the tax rate on the gains down to ~20%. So at least as currently implemented, and assuming the system is not touched, it’s highly favourable to long-term buy-and-holders.

There isn’t a lot of debate about the capital gains tax. For most Finnish people their private investments are such a small part of their total financial picture that it doesn’t matter to them.

>OVER ONE THIRD (34%) of my savings will be wiped away

Definitely not. Everything you save, you can take out tax-free, the tax only applies on profit. If you invest 1000 €, and sell the investment later for 1 300 €, only the 300 € is taxed

Canada is 50% and theyre actively trying to make it 65%, one of the reasons I moved here. There are legal ways around it if you know about holding companies and trusts and starting a part time business. A good accountant who knows the laws will understand what you should do.

I wouldn’t mind capital gains tax being more progressive. Now there are just 2 levels, 30% or 34%.

However, the government will not just ‚take away 34% of your savings‘. It’s unlikely that all your future withdrawals from stocks/funds/ETFs would be gains. Part of it is your original contribution, which will not be taxed. Also, if you hold an asset long term (more than 10 years), you can use ‚hankintameno-olettama‘ which will lower the tax burden. In my own projections I assume I’ll pay 20-25% tax on my asset withdrawals in the future.

As a last note, hard to say will the tax brackets change. At the moment there doesn’t seem to be any strong movement for lowering them.

I am not really an average citizen, but have considerable investments.

It is not terrible currently as we have hankintameno-olettama which can cut down taxes on long term investment by up to 40% for 10-year investments if you have done well. I think this is something mostly unique to Finland?

But the risk is real for increases, wealth tax, exit tax. Because the economy and govt budget balance is in the toilet, and that will be seen as a potential avenue to help the situation somewhat especially on the left.